Whirlpool Corp Stock: Buy For Dividends, Growth, And Value (NYSE:WHR)

Written by ABC AUDIO on February 3, 2022

Neilson Barnard/Getty Images Entertainment

Whirlpool Corporation (WHR) is a buy for long-term investors seeking dividends, future growth, and current value. The market rarely offers high-quality companies with above-average dividend yields at below-average prices. Fewer of these companies offer consistent growth spurred by secular consumer demand trends. Whirlpool is one such company.

Work-from-home trends permanently accelerated due to the ongoing COVID situation. Relative to demand, global single-family home inventory is limited. As a result, home prices jumped in 2021. Further pricing gains will spur unremitting consumer investment into the most used and visible areas of the home. With the most popular brands in America, Whirlpool directly benefits from these dynamics. Domestic revenue increases, the pricing power to counteract inflation, and re-focused international operations will contribute to enduring earnings growth for the business.

Down 20% from all-time highs with a 2.73% dividend yield and a 7.7x P/E ratio, Whirlpool management projects continued earnings growth for 2022. With a consistent emphasis on margin improvement and robust shareholder returns, I consider WHR significantly undervalued. Persistent demand for Whirlpool products will propel future earnings growth and eventual re-rating of pricing multiples for the WHR stock. Whirlpool is currently under-appreciated by the market. Consequently, investment at today’s prices offers a sizable margin of safety. Patient shareholders stand to benefit from future dividend growth and robust capital gains.

Whirlpool Business Background

Products and Brands

Walk in to your kitchen or laundry room. Odds are good that Whirlpool manufactured at least one of your appliances. It may not say Whirlpool, but the company produces appliances under multiple names. Price points and features range from high-end brands to economy models:

Appliance brands manufactured and sold by Whirlpool, domestically and internationally.

The company claims a commitment to being “the best global kitchen and laundry company”. Based on reputation and popularity in the United States, KitchenAid is King of the Kitchen and Whirlpool Washes Away the Competition (I made those up, I should be in marketing!). In possession of the most popular name brands, WHR garners a marketing edge relative to competitors General Electric (GE), Samsung, and LG. Although WHR’s Maytag and Amana brands are less popular, they have a reputation for reliability, dependability, affordability, and value. In contrast, Jennair sells high-end kitchen appliances for those with more refined tastes and a desire for designer fashion. Metaphorically speaking, Whirlpool Corporation offers brands for Growth and Value home appliance “investors”.

International Operations

WHR is truly a global company. Sales of international products come under the Bauknecht, Indesit, and Hotpoint brand names. With manufacturing operations in Europe, Brazil, India, and Russia, the company supplies most high-growth international markets. International markets contributed 43% of total 2021 revenue, but only 16% of Earnings Before Interest & Taxes (EBIT). North America clearly offers greater profit margins relative to international markets.

Fiscal year 2021 revenue, earnings, and margins by area of operations. Created by the Author

While EBIT margins are lower internationally, Latin American and EMEA (Europe, Middle East, Africa) markets showed superior revenue growth in 2021 at 22% and 16%, respectively. These compared to 11% for North America. While less profitable than North American markets with respect to total net income, future international revenue growth will likely boost long-term earnings for the broader company.

International Sales & Acquisitions

In 2021, WHR made several strategic changes as part of an effort to improve return on invested capital of international operations. In Asia, WHR divested its operations in Whirlpool China, which included a 51% interest in joint-venture Galanz. Further, WHR sold its Turkish operations in 2021. Between unconventional Turkish monetary policies and deteriorating support for a capitalist economy in China, these two countries are a hot mess. With leadership changes in these countries unlikely, I view the divestitures as a net positive for WHR. Good riddance.

On the positive side, Whirlpool Corporation increased its ownership stake in Elica P.B India from 38% to 87% for a cost of $57 million. The business emphasizes kitchen appliances and promises relatively “high ROIC and accretive returns”, per the Q3 Whirlpool shareholder presentation. India represents a far more stable environment for business investment and brings the benefit of continual increases in per capita disposable income. A fertile ground for continued revenue growth.

U.S. Housing and Product Demand

The long-term investment thesis for WHR requires discussion of a few critical factors driving demand for home appliances in the United States. While international operations remain important for business growth, the vast majority of Whirlpool Corporation earnings derive from domestic sales. Success in the U.S. means success for the Whirlpool business and WHR shareholders.

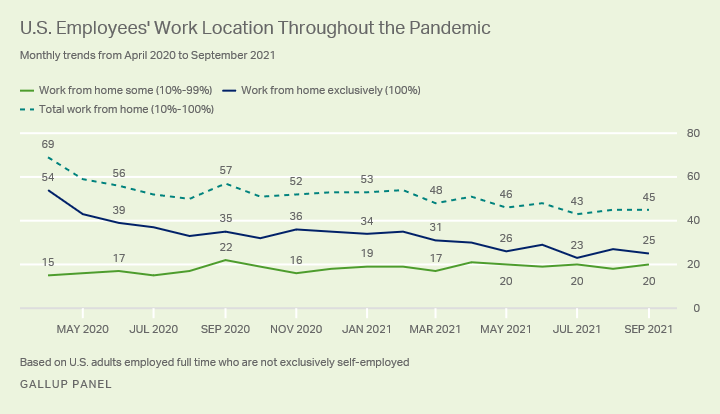

Work-From-Home Trends

The 2020-2021 COVID outbreak necessitated an increase in the proportion of employees working from home. This fact underpins multiple trends for housing demand and housing upgrades. Notably, the proportion of employees working from home at least part-time continues to increase since the beginning of the pandemic. This whole Work From Home movement is not going away. As a result, employees increasingly use their kitchen appliances. This boosts the desire for appliance upgrades. In steps Whirlpool to satisfy the demand.

Percentages of U.S. employees working from home exclusively and part-time.

Home Sales

Increasingly flexible work locations drive additional dynamics. First, employees spend more time at home and no longer need to live in an urban area close to the office. Since the pandemic began, single family home demand substantially increased and home sales went wild. Although sales growth subsequently decelerated, home demand remains strong. As such, demand for new Whirlpool products remains strong.

New home sales totals presently sit well below levels prior to the Great Financial crisis. New home sales growth has a lot of catching up to do, and Whirlpool products will help fill the void.

Future home demand shows no signs of slowing as families take advantage of employment flexibility and move to the suburbs in pursuit of greater living space. Additionally, greater numbers of hispanics and millennials began searching for homes outside of the city. Home sales are forecast to rise further in 2022. See the recent market forecast from Realtor.com for a full discussion.

What’s the point of housing sales trends? New homes must be furnished with new appliances. As the most popular appliance maker in the U.S., WHR benefits from rising home sales.

Home Remodels

Along with the exodus to the suburbs and swelling home sales, the frequency of home remodels generally increases. Whether buying or selling an existing home, remodels require a significant investment. Kitchen remodels provide a high return on that investment, with the average return on investment for a kitchen remodel ranging from 93% to 99%. In the home remodel space, that ranks near the top of the charts. For those looking to sell their home, a remodeled kitchen is one of the most highly sought-after features for prospective buyers. Upgraded kitchen appliances inevitably come as part of the renovation, complete with new Whirlpool products.

Whirlpool Demand Forecasts

In the end, between simple appliance upgrades, new home sales, and existing home renovations, the robust demand outlook for new durable consumer goods persists. WHR management anticipates 4% annual growth in replacement appliance demand. This figure doesn’t include product sales for new homes or growth of international operations.

WHR projects 4% annual growth of U.S. demand for replacement appliances.

Financial Profile and Earnings History

Credit Rating and Debt

Whirlpool Corporation currently possesses an investment-grade credit rating of BBB from S&P Global. The company’s long-term debt/equity ratio sits at 37%. Net total long-term debt rose in the 2014-2019 period. During that time, stock buybacks were prioritized, with net buybacks commonly in the range of $200 million per quarter.

WHR total net long term debt since 2006. Seeking Alpha

Since late 2019, net long-term debt levels significantly dropped as profitability surged. The company paid off debt and accumulated cash. Despite spending greater than $1 billion in stock buybacks during fiscal year 2021, the debt profile improved substantially. In quarterly earnings presentations, management notes that the gross leverage ratio currently resides below the target of 2.0x.

Regardless, the debt profile of the company appears quite manageable, as the current ratio sits well above 1.0 and no liquidity issues are apparent.

Revenue, Earnings, and Margin Trends

Since 2006, across two recessions and an epic collapse of the housing industry, WHR increased annual revenues 56%. This equates to a compound revenue growth rate of approximately 3% annually. Not excellent, but still positive.

Cumulative revenue increase for WHR since 2006, showing an inconsistent but a broadly increasing trend. Seeking Alpha

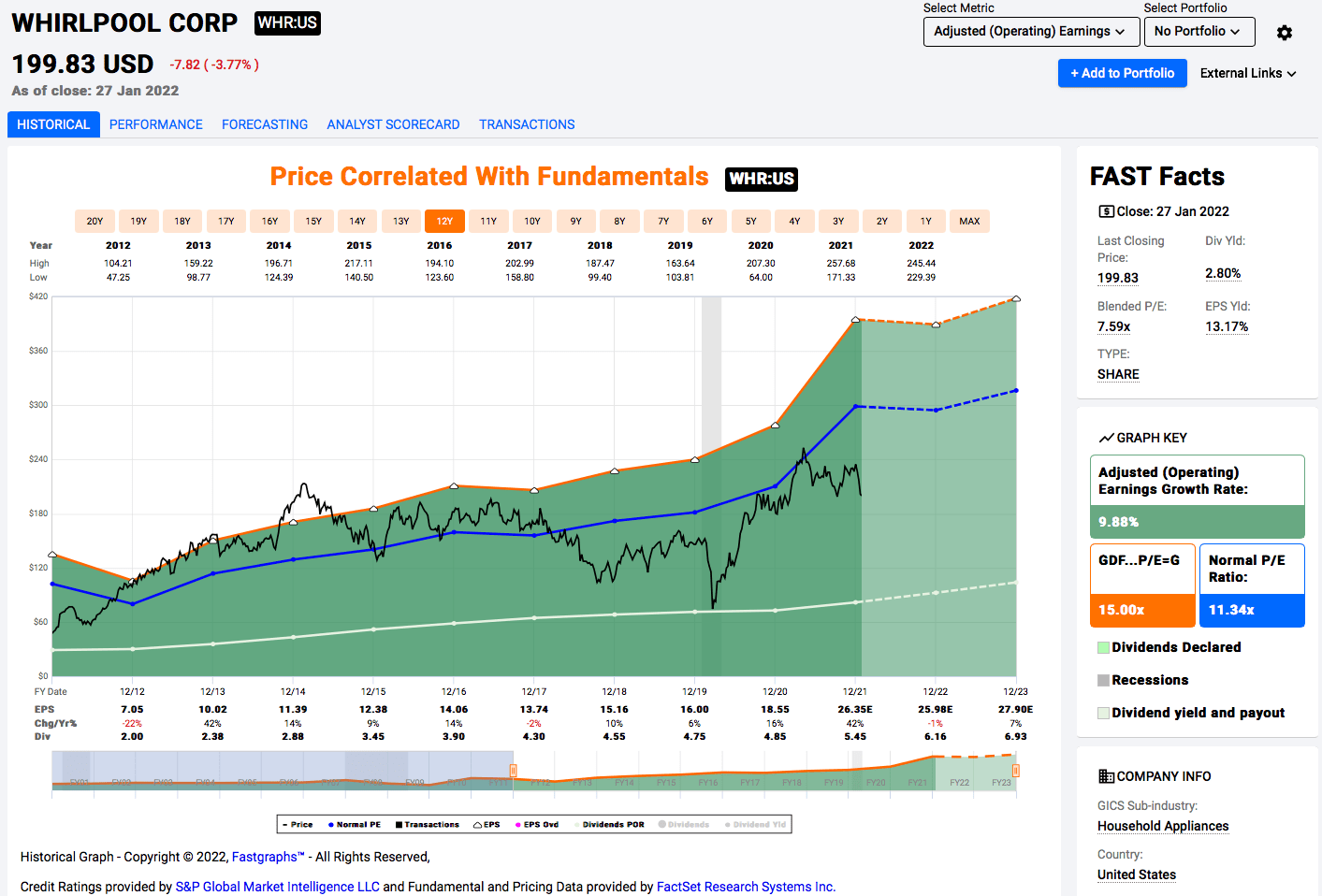

Since exiting the Great Recession and recovery of the housing market, net income rose 470%. Ten-year adjusted earnings since 2011 grew at a 9.8% compound annual growth. A significant portion of this growth occurred during fiscal year 2021. However, even without the banner year of 2021 included, earnings growth compounded at 8.35% annually. Not too shabby.

WHR stock price, dividend, and adjusted earnings history since 2011. The orange line represents a 15x P/E multiple of annual earnings. The blue line represents the historical average P/E ratio during this time of 11.3x. FastGraphs.com

Net income and earnings per share rose a much greater pace than revenue as a result of two factors. First, stock buybacks clearly had an impact, as total share count decreased 22% over the prior ten years. Second, net income margins (profit margins) showed broad improvement from <2% in 2012 to greater than 8% in 2021.

Net income margins (profit margins) since 2012. Seeking Alpha

Are these profit margins sustainable? I believe so. While profit margins undeniably improved during the COVID shutdowns, margins reached nearly 6% in late 2019, before the pandemic hit. In addition, management recently issued strong guidance for their preferred measure, Ongoing EBIT Margin. This represents profit margins before interest and taxes on a trailing twelve month basis.

WHR Ongoing EBIT profit margins since 2007, with management targeting 11-12%. Whirlpool Corp Investor Relations

For fiscal year 2022, management expects a full-year Ongoing EBIT margin of 10.5%. The rationale for continued strong margins rests on cost controls, increased productivity, and investment in higher return on capital areas. Further, continued strong housing demand and remodeling trends will support current levels of profitability.

Free Cash Flow and Dividend History

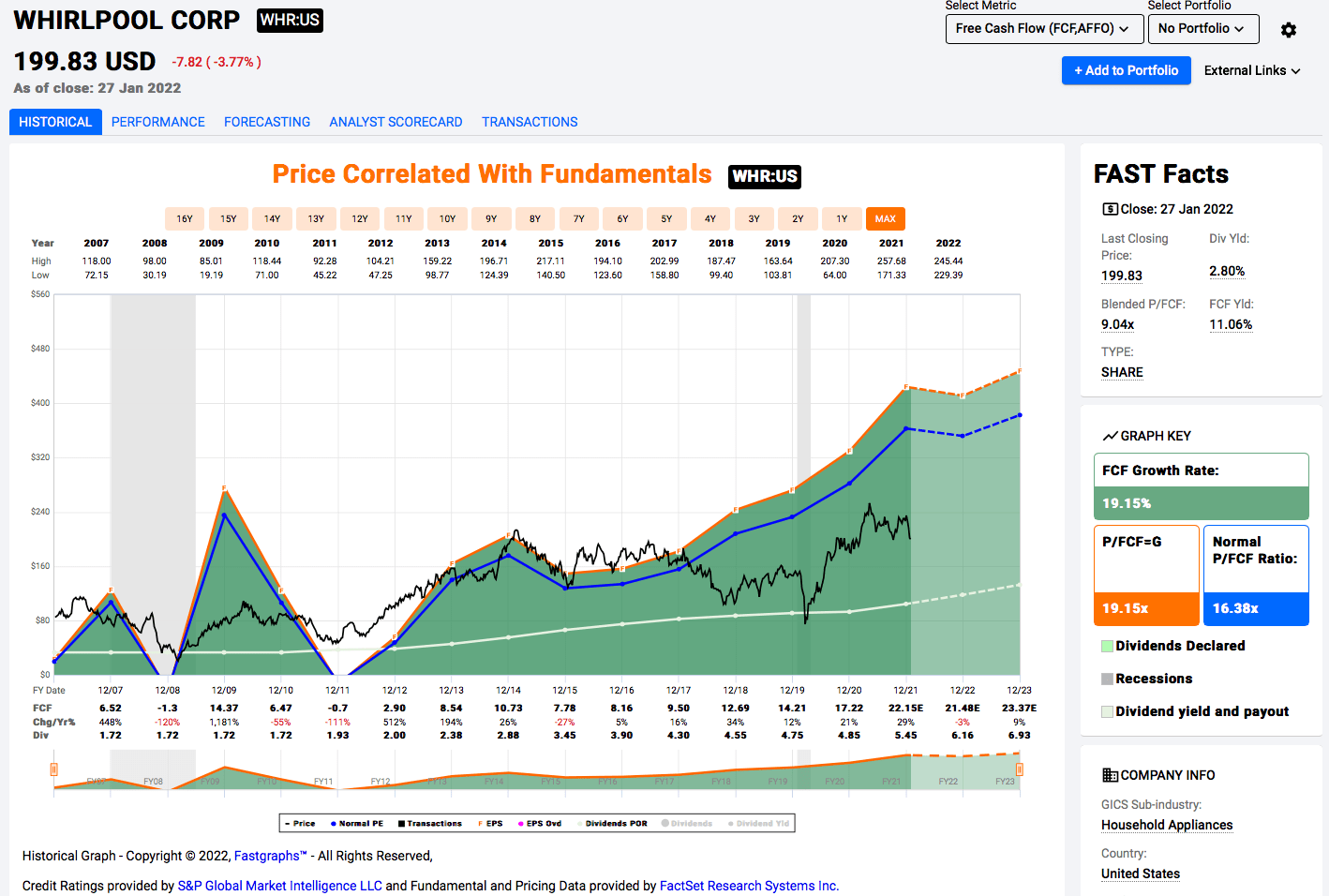

Whirlpool Corp is arguably a more consistent and stable company since exiting the Great Recession and housing crisis. The image below shows price and free cash flow trends since 2006:

WHR price, dividend and free cash flow history since 2006. The blue line represents a historical average Price / Free Cash Flow multiple of 16.4x during that time. FastGraphs.com

Prior to 2013, free cash flow was highly erratic. Dividend growth was non-existent prior to 2011. Including the Great Recession and housing bust, free cash flow grew at a 19% compound annual growth rate. Moreover, since working through the housing crisis, free cash flow trends reliably exceeded annual dividend payments. Post 2012, free cash flow growth continued at a 20% annual average pace and typically exceeded 10% annual growth.

Dividends grew alongside free cash flow at an 11.8% compound annual growth rate. For reference, an investment in late 2012 at a dividend yield of 1.97% resulted in a current yield on cost of 6.0%.

Investment Performance

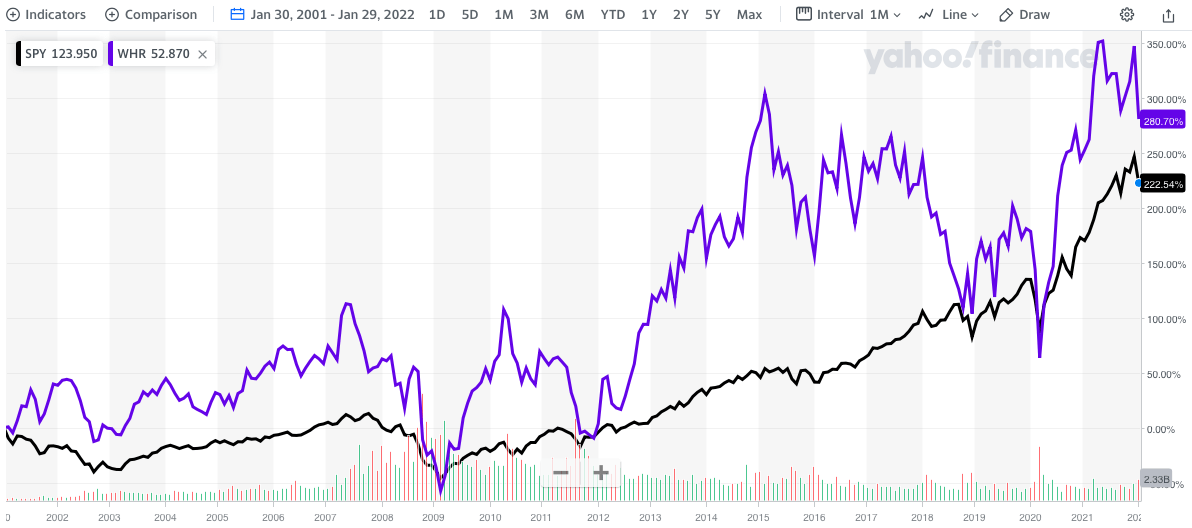

As measured against an investment in an S&P 500 Index ETF (SPY), the returns of WHR stock have been poor to excellent. As always, it depends on the timeframe measured. 1-Year returns favor SPY, whereas 2-year pricing returns are nearly identical at 37%. 5-Year returns favor SPY by a large margin, but WHR wins on 10-year returns by > 40%.

For reference, here is a 20-year plot of WHR stock price vs the S&P 500, represented by SPY:

Pricing comparison of WHR vs SPY since 2001.

An investment at the beginning of 2001 produced annualized total returns of 8.3% for Whirlpool versus 6.9% for the S&P 500. I, for one, would take that performance. I also believe that future returns in WHR will be much improved relative to this period, because the prospects of another housing and financial crisis are relatively low. Further, current pricing multiples work in the investor’s favor.

Also of note: WHR stock experienced dramatic drawdowns in 2009, late 2011, late 2018, and early 2020. An investment at these times produced annualized returns through today of 19%, 17%, 22%, and 45%. During each of these periods, WHR stock traded at P/E ratios below 8x. The same valuation is available today. See the FastGraphs plots from above for reference.

Current Valuation

Trailing Metrics

Based on trailing twelve month earnings from Yahoo Finance, WHR trades at a current P/E of 7.24. Compared against a 10-year historical P/E average of 11.3x, this represents a discount to fair value of -36%. The 20-yr average P/E ratio comes in at 11.6x. Relative to earnings, WHR stock is a fantastic value.

Turning to EV / EBITDA, the company trades at the low multiple of 5.4x versus a typical value near 8x. This works out to a fair value discount of approximately -30%. Using this metric, WHR shares haven’t been this cheap since the March 2020 COVID lows and mid-2012 prior to that. Remember, those were the periods which produced approximately 20% annualized total returns to present day.

EV / EBITDA ratio for WHR since 2012. The current value sits at 5.4x Seeking Alpha

Using managements preferred measure, EV / EBIT, which doesn’t account for depreciation, WHR appears even cheaper with a rock-bottom multiple of 6.55x. One must search back to the bargain-filled days of 2011 to find a period of time in which the company was cheaper than current levels.

Forward Metrics And Free Cash Flow

Analysts project a -2% drop in 2022 earnings relative to 2021, from $26.59/share to $25.98/share. I suspect WHR share pricing reflects a decrease in EPS profitability over the next few years. Generally speaking, the market does not believe that recent revenue and margin performance can be sustained.

However, in the most recent earnings call, management issued fiscal 2022 earnings and free cash flow guidance. The company expects earnings per share to range $27-$29 / share. Thus management anticipates earnings growth of 1.5% – 9.0%. This equates to a forward P/E of 7.1x – 7.6x. Low-end and high-end ranges for the guidance reflect uncertainty regarding ongoing supply chain constraints. Regardless, forward P/E ranges are historically cheap on a forward basis.

Neilson Barnard/Getty Images Entertainment

Long-term goals and 2022 guidance metrics. Whirlpool Corp Investor Relations

While future free cash flow may drop from $1.7 billion down to $1.5 billion, revenue projections continue to climb. After implementing a 5% product pricing increase to counteract inflation, margins will remain strong for 2022. The current pricing discount of WHR stock is simply not merited based on current and future business performance.

Regarding upcoming dividends and buybacks, the company guided for 2022 cash returns to shareholders of $1.5 billion. WHR paid $338 million of dividends in 2021. Given these figures, I anticipate another strong dividend increase from WHR in April 2022, following up on the 10% dividend increase in 2021.

Investment Return Estimates

Here I’ll project a range of outcomes for 2-year investment returns. For the base case, I’ll assume price reversion to a 20 year average fair-value P/E ratio of 11.6x. On the low end, we’ll premise the market doesn’t re-rate WHR and the stock trades at an 8x P/E ratio. For the high case, consider the possibility of WHR reaching a 15x P/E ratio, as occurred frequently during the 2013-2015 time period.

- High Case 2-Yr Returns = 110% Total Return or 47% Annualized

- Base Case 2-Yr Returns = 63% Total Return or 29% Annualized

- Low Case 2-Yr Returns = 15% Total Return or 8% Annualized

These values rely on current analyst estimates for fiscal year 2023 earnings ($27.90/share). Current undervaluation of WHR stock substantially improves the base case and high case return estimates.

In the long run, the buy-and-hold investor can expect continuation of the 9-10% CAGR of earnings, plus a 2-3% dividend. Ultimately, I see 10-12% annualized returns over the course of a decade or longer as entirely reasonable.

Whirlpool offers current value, long-term structural growth, and above-average dividends.

Dividend Growth Estimates

Although the company lacks the dividend pedigree of some dividend champions, WHR’s 12-year dividend increase streak remains intact. Projecting into the future, I believe WHR will continue to prioritize dividend growth and shareholder returns. The current payout ratio works out to 20% of adjusted earnings and 24% of free cash flow. As such, the scope for further dividend growth is sizable.

The chart below offers a range of future dividend growth rates across the full business cycle (recessions included):

Potential yield on cost estimates for an investment in WHR at current stock prices. Created by the Author

The low case implies a collapse of the housing market and retrenchment of WHR growth. The high case considers expanded housing construction to increase inventory and fulfill rising global demand. The base case extends the history of the prior decade into the future, with a small debit for recessionary slow-downs.

Stated another way: at 9% dividend growth, a $10,000 investment in WHR could produce over $9,000 of cumulative dividend income through the course of 15 years. For extra compounding, dividend reinvestment would generate nearly $11,500 of total dividend income.

Investment Risks

I see three primary risks associated in a Whirlpool Corp. investment.

First, continued supply chain pressures may inhibit product availability and suppress revenues. Management outlined this scenario in the Q&A of the recent earnings call. I suspect price increases could counteract increased product scarcity.

Second, EBIT profit margins might collapse down to historical levels of 8% or less. While within the realm of possibility, executives at the company clearly have a focus on maintaining cost efficiencies and allocating capital to higher return areas of the globe. I view this risk as unlikely, but not negligible.

Third, a collapse of the housing market could appreciably crimp product demand. Why might this occur? Over-zealous rate hikes from the federal reserve might potentially (1) raise mortgage rates to undesirable levels, or (2) cause a recession. Either case would suppress the housing market and reduce appliance purchases. After navigating the Great Recession, the financial crisis, and a destructive housing market bust, I believe WHR management to be capable of handling this situation when it occurs.

Regardless, WHR investors must be prepared for stock price volatility associated with fluctuating economic conditions. This company is one to buy for the long term, but the ride may be bumpy on the way. Maintain sanity by enjoying the dividend income!

Conclusions

Whirlpool stock is a buy for value, for growth, and for dividend growth. The stock trades at unjustified, bargain pricing levels based on the P/E ratio, EV / EBITDA ratio, and forward earnings estimates. The stock is priced at a -30% discount to fair-value, as if future profit margins and earnings will collapse. This assumption runs contrary to recent management guidance, which suggests continued growth. Simple price reversion to historical earnings multiples could provide outstanding near-term capital gains to the tune of 60% over two years. Additionally, strong dividend growth is likely to reward income-oriented investors.

Over the long term, continued global growth for new housing demand promises an enduring runway for WHR products. Domestically, the permanence of work-from-home trends and the exodus to the suburbs will spur continued new home sales growth with increased existing home remodels. This dynamic is a structural tailwind for WHR product demand. As a buy-and-hold company, investors should expect continued growth with approximately 10-12% annualized total returns over the course of decades.

— to seekingalpha.com

The post Whirlpool Corp Stock: Buy For Dividends, Growth, And Value (NYSE:WHR) appeared first on Correct Success.